Rising Interest Rates Are Trapping Texas Homeowners — Here’s Your Exit Strategy

Introduction: The Interest Rate Trap

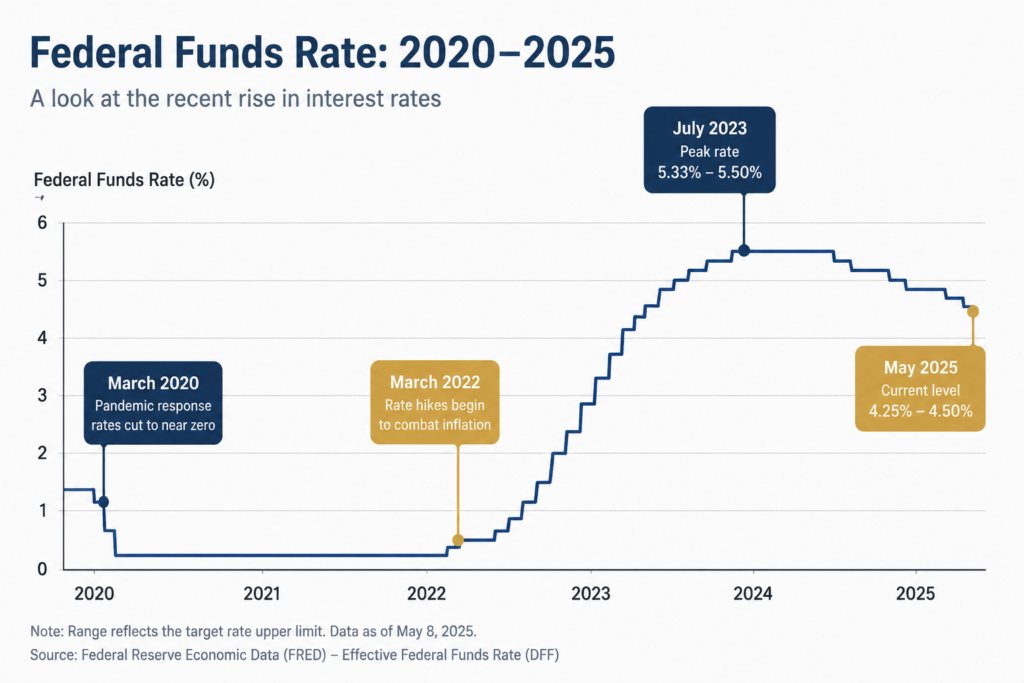

From 2020 to 2021, mortgage rates hit historic lows — hovering around 3%. Millions of Americans, including thousands of Texas homeowners, took on new mortgages, refinanced, opened home equity lines of credit (HELOCs), or took second mortgages at those low rates. It felt like free money.

Then, beginning in March 2022, the Federal Reserve began the most aggressive rate-hiking cycle in four decades. By mid-2023, the federal funds rate had climbed from near-zero to over 5% — and mortgage rates followed, pushing past 7% and 8% for conventional 30-year loans. For homeowners with variable-rate products, the change was sudden, dramatic, and in many cases, financially crushing.

If you’re one of the Texas homeowners caught in this rate environment — with an adjustable-rate mortgage that’s repriced, a HELOC with a ballooning payment, or a financial situation that simply no longer pencils out at today’s rates — this guide is written for you.

What Changed and Why It Matters for Texas Homeowners

The rate environment since 2022 has created several distinct financial pressure points for homeowners:

Adjustable-Rate Mortgages (ARMs) That Have Reset

Many homeowners took out 5/1 or 7/1 ARM loans in 2017–2020, believing they would refinance or sell before the adjustable period began. When rates were low, that made sense. Now, those loans are resetting to current market rates — in some cases adding $800 to $1,500 per month to a mortgage payment overnight. For households on fixed incomes or tight budgets, this is a financial shock that can lead quickly to default.

HELOCs with Variable Rates

Home equity lines of credit are almost always variable-rate products tied to the prime rate. A HELOC opened in 2021 at 4% may now be charging 9% or higher. For homeowners who used their HELOC for renovations, education, or consolidating debt, these payments have ballooned well beyond the original plan.

The 'Locked In' Effect and Its Reverse

Ironically, homeowners with low fixed-rate mortgages (3–4%) have been reluctant to sell because doing so means giving up that rate and taking on a new mortgage at 7%+. This has contributed to Austin’s inventory crunch. But for homeowners whose financial circumstances have changed — job loss, divorce, health expenses, retirement — the locked-in effect works against them: they need to sell, but feel paralyzed by what comes next.

Who Is Most at Risk in Today's Rate Environment?

In our experience across Central Texas, these homeowner profiles are most likely to be feeling the squeeze:

- ARM borrowers with 2018–2022 loans: Their initial fixed period has ended or will end soon, and the reset payment is dramatically higher than anticipated.

- Retirees with HELOCs: Many retired homeowners supplemented fixed incomes with HELOC draws that are now expensive to service.

- Self-employed buyers from 2020–2021: Texas saw a surge of relocations and purchases from remote workers. Some of those income situations have changed — remote roles eliminated, companies recalling workers to other cities.

- Multi-property holders: Landlords who bought investment properties at 3–4% and now face mortgage renewals or HELOC resets are finding the numbers no longer work.

- Couples with combined incomes that have dropped: Divorce, a spouse leaving the workforce, medical issues — any reduction in household income that makes a previously affordable payment suddenly unmanageable.

Your Options When the Mortgage Is No Longer Manageable

If your home payment has become unmanageable, or you can see the reset coming in the next 6–12 months, these are your realistic options:

Option 1: Refinance to a Fixed-Rate Mortgage

If your credit and equity position allow, refinancing your ARM into a 30-year fixed can provide payment certainty. The downside: today’s fixed rates are significantly higher than they were, so refinancing may not meaningfully lower your payment — and closing costs of 2–4% add to the debt.

Option 2: Contact Your Servicer About Hardship Programs

Many mortgage servicers have internal hardship programs — forbearance, temporary rate modifications, or repayment plans — that are not widely advertised. If you’ve had a documented financial hardship (job loss, medical issue, natural disaster), it’s worth asking directly. Success rates vary significantly by lender and loan type.

Option 3: Consider a Loan Modification

A formal loan modification permanently changes your loan terms — potentially reducing the rate, extending the term, or even reducing principal in some government-backed loan programs. This takes time (often 3–6 months) and requires extensive documentation, but can result in a truly sustainable payment.

Option 4: Sell the Home

For many homeowners in the rate trap, selling is the most rational financial decision — especially if:

- Home equity has built up over years of ownership and appreciation

- The payment reset will cause financial hardship within the next 12 months

- Other financial goals (relocation, downsizing, retirement, investment) would benefit from releasing the equity

- A forbearance or modification is not available or not sufficient

Why Selling to a Cash Buyer Makes Sense in This Market

In a high-rate environment, listing your home on the open market introduces new risks that didn’t exist when rates were low:

- Buyer financing fallthrough: When rates are high, financed buyers frequently lose their pre-approval or back out when rates move. A cash sale has no financing contingency — it’s a certainty.

- Longer days on market: Austin’s housing market has slowed considerably from its 2021 peak. Homes are sitting longer. If you’re racing against an ARM reset date or a looming default, a 90-day listing window is a risk you may not be able to absorb.

- Carrying costs: Every month your home sits listed, you’re still paying the high mortgage payment. A fast cash close eliminates weeks or months of that financial drain.

Wayne Sells Houses offers cash offers that close in 7–21 days — with certainty. There are no open houses, no agent negotiations, no financing contingencies, and no waiting.

Using Equity as Your Exit Ramp

Here’s the financial reality that many homeowners in this position don’t fully appreciate: despite the rate environment, most Central Texas homeowners who bought before 2022 still have substantial equity. Austin-area values, while corrected from their 2022 peak, remain dramatically above 2019 and 2020 levels.

If you bought a $350,000 home in 2019 and it’s now worth $480,000, you have equity — even after paying off the mortgage. That equity is real money. And every month you delay selling (and paying that high ARM payment), you’re eroding your net position.

A cash sale captures that equity now, before further rate resets or market softening reduce it further.

Questions to Ask Yourself Right Now

Use these questions to honestly assess your situation:

- If my ARM resets at the current index rate, can I still comfortably make the payment?

- Do I have 6–12 months of financial reserves if something else goes wrong?

- If I listed my home today and it took 90 days to sell, could I bridge that gap financially?

- Is staying in this home aligned with my goals for the next 3–5 years?

If the honest answer to most of these questions is ‘no’ or ‘I’m not sure,’ it’s worth at least having a conversation about what a cash sale would look like for your specific situation.

No Pressure, Just Options: Talk to Wayne Today

Wayne Morgan has been helping Central Texas homeowners navigate financial pressure with dignity and respect since 1985. He’s seen interest rate cycles before — and he knows that the homeowners who make deliberate, proactive decisions almost always end up in a better position than those who wait and react.

A conversation with Wayne costs nothing and commits you to nothing. You’ll get a clear picture of what your home is worth, what a cash offer would look like, and whether selling now makes financial sense for your situation.

Call (512) 997-8457 or fill out the form at waynesellshouses.com. Knowledge is power — and right now, the more options you understand, the better positioned you are, whatever you decide.